Profile

| Sector | Water |

| Gross Value Added, 2023 (£bn) | £16.2 billion |

| Number of workforce jobs, 2024 | N/A |

| Key projects | Thames Tideway Tunnel, Haweswater Aqueduct Resilience Programme (HARP), Dŵr Cymru’s Cwm Taf water treatment works |

| Key UKRN regulators | Ofwat |

| Regulatory approach | Ofwat sets sector’s funding envelope at company level every five years, through the Price Review (PR) process |

Water is essential to life, and every day over 50 million consumers in England and Wales receive good quality water, sanitation and drainage services. These services are provided by privately-owned companies in England and Wales.

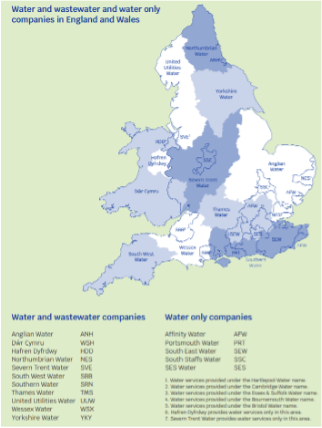

There are 28 appointed companies, of which 16 are regional monopolies that provide either water services (water only companies, WOCs), or both water and sewerage services (water and sewerage companies, WASCs). The companies vary significantly in size – there are 11 larger WASCs and five smaller WOCs. There are also 12 small water and sewerage undertakers providing services to specific sites or small geographic areas and one licenced infrastructure provider delivering the Thames Tideway Tunnel.

There is also a single state-owned company that supplies both water and wastewater services in Scotland (Scottish Water). In Northern Ireland, water and wastewater services are provided by Northern Ireland Water, which is regulated by the Utility Regulator for Northern Ireland (UR).

Households are not able to choose their water supplier, but the business retail market in England and Wales was opened to competition on 1 April 2017, and eligible non-household premises are no longer restricted to buying water and sewerage services from their regional monopoly.

As set out in the National Infrastructure Commission’s Second National Infrastructure Assessment, at least 1,300 mega litres of water per day will be needed by the mid-2030s. Meeting this challenge requires a step change to both increase water supply and reduce water demand, delivered through a combination of new strategic water resource options and ambitious demand‑side measures.

At privatisation, the roles of regulation and the provision of water and sewerage services were separated. Three independent bodies were established to regulate the industry and protect the interests of customers and the environment. These bodies were the National Rivers Authority (subsequently subsumed into the Environment Agency), the Drinking Water Inspectorate, and the Director General of Water Services supported by the Office of Water Services (replaced by the Water Services Regulation Authority in 2006) but known as Ofwat.

The Department for Environment, Food and Rural Affairs (Defra) sets the overall water and sewerage policy framework in England, including standard setting, drafting of legislation, and creating special permits. In Wales, the Welsh Government is responsible for these matters. Regulation has evolved since privatisation, and environmental regulation, drinking water regulation and economic regulation of the water industry in England and Wales is currently conducted by The Environment Agency, the Drinking Water Inspectorate, and Ofwat respectively. The water industry also works closely with a number of other organisations, notably the Consumer Council for Water (CCW), Natural Resources Wales and Natural England.

However, the government has recently announced that Ofwat will be replaced with a new regulator whose functions will be merged with water functions across the Environment Agency, Natural England and the Drinking Water Inspectorate to form a new single regulator for the whole of the water sector. These proposals are included in a White Paper published by Defra in January 2026, which will form the basis of a new Water Reform Bill, to be introduced to Parliament. A separate green paper was published in February 2026 by the Welsh Government which describes the basis of future water regulation in Wales.

One of the ways in which Ofwat regulates is to set the price, investment and service package that customers receive, including setting controls that limit what companies can charge their customers. Ofwat carries out a review of these price limits every five years, issuing final determinations in the PR24 process in December 2024, effective for the period April 2025 to March 2030. The determinations included within PR24 are intended to support a total expenditure of £104 billion over the five-year period and include an allowed return of 4.03% (in real, CPIH terms).

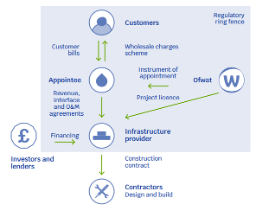

The main investment opportunity is the Major Water Infrastructure Programme, which is a pipeline of 30 major infrastructure projects that will be put out to tender for competitive delivery (including detailed design, building, operation and maintenance) by third parties – and largely sit outside of the price review process. Major projects are defined as those with a whole life total expenditure (‘totex’) exceeding £200 million and meeting the criteria for delivery through Ofwat’s competitive tender models, either Direct Procurement for Customers (DPC) or Specified Infrastructure Provider Regulations (SIPR) – see below.

Direct Procurement for Customers (DPC) structure

Specified Infrastructure Provider Regulations (SPIR) structure

Ofwat’s Major Projects directorate works closely with Regulators’ Alliance for Progressing Infrastructure Development (RAPID), which is a regulatory alliance made up of the three water regulators Ofwat, Environment Agency and Drinking Water Inspectorate. Together they are responsible for the policy and market development of future pipeline of major infrastructure projects in the water sector in England and Wales, as well as Ofwat’s role in the oversight of the development, procurement, and delivery of these projects.

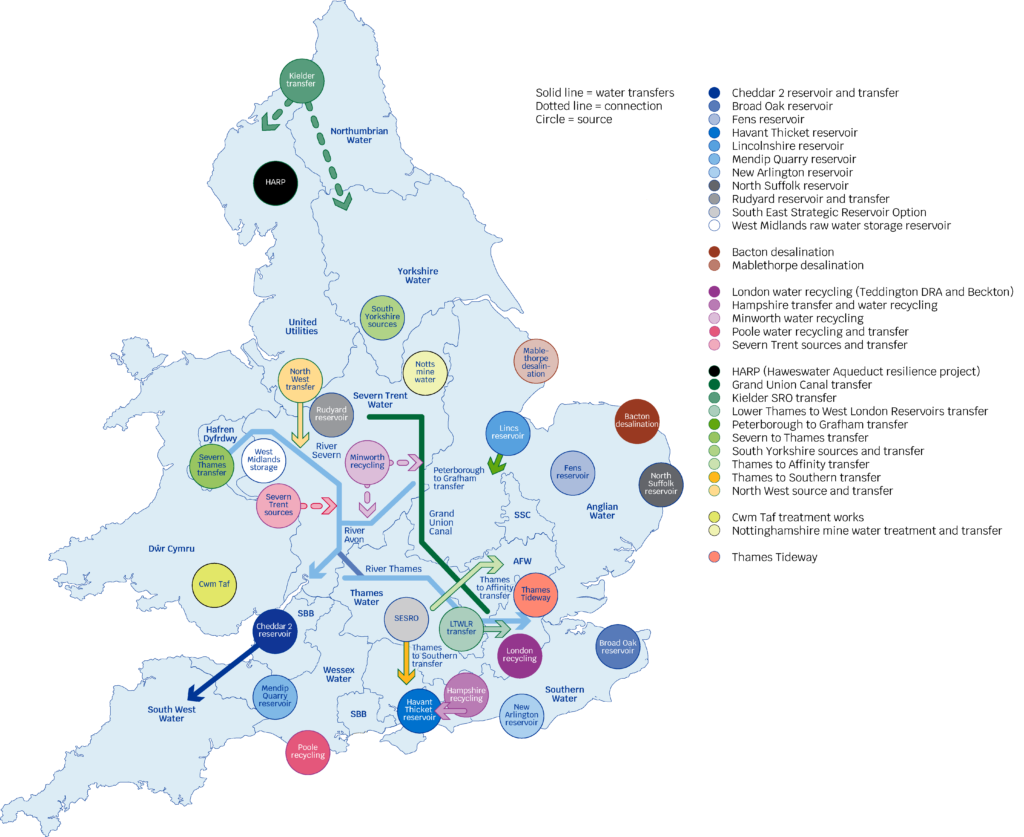

Ofwat’s PR24 final determinations accepted a portfolio of around 30 major projects (see map below), with a totex across all projects estimated at upwards of £50 billion (2022-23 prices). Recent analysis commissioned by Ofwat estimates that the one-off impacts of the investment associated with these major projects is an increase in Gross Value Added (GVA) of £28bn to £41.1bn and peak job creation of 32,000 to 47,000. Although these impacts are expected to be temporary, over the longer term these projects are estimated to increase growth in 2050 by between $4.75bn and £12bn.

These are in addition to three existing major projects – the Thames Tideway Tunnel, United Utilities’ Haweswater Aqueduct Resilience Programme (HARP), and Dŵr Cymru’s Cwm Taf water treatment works, all have been or are being competitively procured and delivered through SIPR or DPC.

Major Water Infrastructure Programme – map of key projects

Ofwat provides a range of information and guidance relevant to analysts, investors and contractors:

- An investor information page, compiling analyst briefings, conference calls and investor roundtables.

- An information page for investors and supply chain partners, providing more detail on the investment opportunities available, plans for market engagement and details about RAPID.

- A guide to Ofwat’s major projects, for both supply chain partners and investors, setting out the role of RAPID, DPC and SIPR delivery models and detailed information about upcoming major projects.